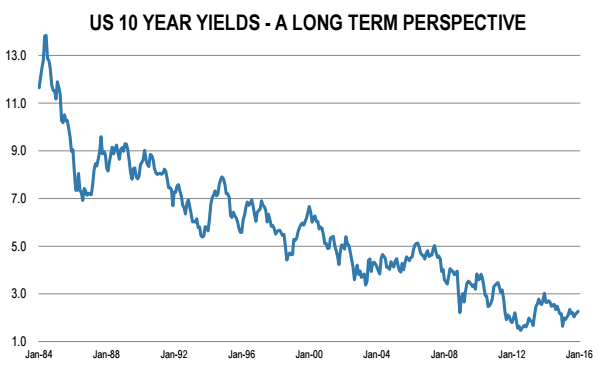

The incredible bull market in bonds

“You seem to have this nasty habit of surviving, Mister Bond”

When Kamal Khan tells James Bond that he has a nasty habit of surviving in “Octopussy” in 1983, he does not refer to the bond market obviously….. But funny enough the year the movie was released more or less corresponds to the start of one of the longest bull markets in history, precisely on bonds.

At the end of the year 2012 one could have thought that good days were over and that being a bond investor, in particular on 10 year Government benchmarks, would become quite a challenging job. At that time markets were increasingly expecting the end of Quantitative Easing by the Federal Reserve, and a progressive “normalization” of the structure of the US yield curve. The reasons were pretty straightforward: self-sustained economic growth, better global growth prospects, improving housing and job markets, strong banking sector, and the list goes on.

The natural path of US government bonds yields was clearly on the upside, and a steepening of the yield curve was widely expected… and happened as US 10 year yields more than doubled from a low of 1.38% in July 2012 to a high of 3.05% in January 2014, a period during which the Fed talked a lot but barely acted (no changes were made on the interest rates side, but QE program was gradually tuned down).

Since then a new sequence of strong performance occurred on the bond side, with US 10 year yields falling back to 2% (as of January 2015) with a short incursion into the 1.60-1.70% zone at the beginning of 2015. What has happened to push yields to such low levels again? Here also the reasons seem quite obvious with hindsight: the initial big down move was triggered by the first spectacular fall in oil prices which started in July 2014 and ended at the beginning of 2015 (from $108 to $42 per barrel), perfectly matching the US 10 year yield move from 3.05% to 1.64%. The second round of falling yields started in June 2015 and is still in place today….there again perfectly correlated to the second round of falling oil prices.

On top of this spectacular fall in oil prices one can add the considerable weakness in almost all commodity prices, so there seems to be a logical reaction from fixed income markets which are anticipating non-existent inflationary – or even rising deflationary – pressures.

Another striking correlation comes with the Chinese Renminbi which peaked in January 2014 (like oil and US 10 year yields) at 6.04 per USD and has fallen to 6.58 per dollar since then. This is a very important event because there are now serious fears that China is on its way to let its currency depreciate further, which would certainly generate a wave of deflationary pressures around the globe.

What can be expected from now on with bonds? With such low levels the risk/reward proposal still appears unattractive and it seems to make more sense to invest on relatively short maturities (maximum 5 years) in order to roll down the curve while it’s still steep. But what if the doomsayers got it right? The Japanese recent history shows that first it is complicated to fight against deflation once it’s in place, and second that it is a highly risky business to bet against a bond market. Those having made money by shorting JGBs are the very lucky few, everybody else having lost money and patience.

And to remind us that this mid-80s – 2015 period has been exceptional, one quick look at the 30 year benchmark issued by the US Treasury in February 1986 and which matures next month is highly illustrative: with a 9.25% coupon, issued at par and reimbursed at par, an investor would have made a 9.25% return annualized, the maths are simple. During the same timeframe, the SP500 with dividends has compounded at 10.3%, a mere 1% better, but with far much more sleepless nights.

So yes, Mr Bond Market, you have a pretty nasty habit to survive!